A rare Sunday alert coming from me, but I have inside information regarding a phone call placed by CA Governor Gavin Newsom. My sources tell me in the wake of the utility’s continued “zombie apocalypse,” shutting the power off for days with little or no warning, has irked our supreme leader so much he placed a call to Warren Buffett late Saturday night. No official word yet if this is the same “red line” phone Ronald Reagan installed to communicate directly with the Russians, alas here is what I have been told. Newsom has told Buffett he is fed up with PG&E’s lack of competence and morals, to the point that he wants the entire company sold and a new leadership team in place. Buffett has more than enough cash as his investment vehicle “Berkshire Hathaway” to make the purchase. My sources, (notice that’s plural) tell me Newsom wants Berkshire to buy the utility and be taken private. This will cut out as William likes to say the 90-day calendar and other reporting requirements with both Wall St, and the SEC.

Here in lies the problem, as corrupt and incompetent as PG&E is, the governor is acting illegally. He is not a shareholder, or an executive of the troubled utility. The decision to be made about a sale is up to the executives, and then voted on by the shareholders not the Governor. Why is he reaching out before another company has the chance? Is this because the city of San Francisco, where he used to infest as mayor, was rebuffed at their attempt to buy the company last week?

It’s not out of the question as Berkshire owns utilities in Iowa, Illinois, South Dakota, Nevada, and in the United Kingdom. There is no doubt he could be a qualified buyer, but why is the governor contacting him? Were prices discussed? What about concessions from the California Public Utility Commission? Since the governor appoints that board. I am sure a ton of SEC violations are occurring right now. If you are a shareholder…well, you’re getting wiped out, bondholder? Same. Union? You’ll be just fine.

Stay tuned but prepare to see movement on PG&E stock Monday, as this story will leak.

The editorial staff was having lunch at the salsa bar this past Monday and we discussed the goings on in a city which the Blog Father calls his adopted hometown. We discussed a myriad of different topics, arguments ensued, battle lines were drawn, red lines were crossed, and parties had to be separated. However, there was one thing we could all agree on; the City of Elk Grove, California in the Year of our Lord 2019, has finally decided to emerge from its status as a bedroom community and joined the ranks of becoming a real city. After 20 years, we were finally tired of living in the shadows of Sacramento, and with their announcement of a Soccer team coming in, we had to one up them. Boy did we ever, showing nary a regard for the taxpayers or future generations in the process.

Just to bring you up to speed, our city has a renegade history. Upon separating from Sacramento County and incorporating, we formed our own bus service (since rolled back into Sac Regional Transit), formed our own police department (now on its 5th chief of police now), subbed out the trash services because the county was overcharging us (we now pay more for services than the county customers do), built our own dog pound (again county was overcharging us), etc. But a series of moves this past several weeks have us even more flummoxed.

Not to be outdone, we also are now the proud owners of a $70k ribbon tree for the holiday season. That’s funny because we have a Dickens Faire where we light a tree in old Elk Grove. I guess this makes sense because old town has a stigma of being racist (all our council members let this go unchallenged) and I guess we believers get an old Christmas Tree while the non-believers get a $70k ribbon tree. We all know how this story ends, the tree gets vandalized or broken over the next couple years and we have to buy another one or face a certain lawsuit.

Elk Grove Dicken’s Faire

But it gets even better. This past week, our city decided to purchase a 15-acre parcel on the corner of Big Horn Blvd and Bruceville Road in what I would call a rapidly deteriorating part of town. (If you doubt me, drop in at WinCo Foods and check out the clientele.) This property will be used for low income housing, which I am sure is funded by grant money from the state and comes with a threat of build the units or face a fine.

City buys N.E. corner lot for $2.9 million

The biggest problem we, on the editorial staff, have is the process and the price. Local Psycho Lynn Wheat tried to halt the process for further discussion when she was overruled by the entire council, who by the way “allegedly” has two Republicans on it, who claim to be fiscally responsible, allegedly. So, we are going to pay $2.9 million for this plot of land…at the height of the real estate market…for vacant land. However, even more troubling is the purchase price. The current owner bought this plot for $1 million in October of 2017. Check my stats if you want, I’ve attached links. These reeks of a government corruption issue. How can the price of vacant land more than double in 2 years? And not a single one of our council members or our beloved mayor have an issue? Not throwing any accusations, but one member, who doubles as a PG&E Vice President has a spouse who is the best-known realtor in the Sacramento County area. Surely, she would have objected right? My house appreciated in value by, call it $100K in 5 years, but for a blank piece of property to more than double in value I think an investigation should be in order.

Elk Grove Aquatic Park

Add these to our aquatic center opening earlier this summer to major fanfare only for the City to increase entrance fees after deeming then inadequate after 1 weekend. Speaking of inadequate, the same center is up to its armpits in litigation because of defective workmanship. Cost effectiveness and fiscal savvy are clearly not on display.

I guess you can say it pays to be an elected official.

Welcome to the big time Elk Grove, thankfully as William pointed out, our city is “green” according to the auditor’s website meaning our financial health is fine, who knows where this spending puts us. Soon we’ll catch up to everyone else.

The California State Auditor has rested from her labors filtering names for the citizen’s committee on redistricting long enough to release a report on the financial health of California’s cities. The quote on “lies, damn lies, and statistics” comes to mind when you read about Paradise, California being listed at moderate financial risk. Gee, maybe you could put an asterisk on that or something. Last we checked, those folks got their ashes kicked by a small conflagration and then PG&E & their insurance carriers piled on.

Paradise reported at moderate financial risk

If you want a preview of coming attractions, start clicking on the filters on the left side of the interactive map page; especially, Future Pension Costs. Remember that this data is several years old, and the trend is not getting better.

Future Pension Costs –Sacramento

Future Pension Costs –San Francisco Bay Area

I’m so glad that the politicians made sure government employees are in the front of the line when creditors line-up to claim their share of the carcass when all this goes south. Meanwhile, mostly empty lifeboats are departing daily for Texas and other locations.

Now that the evil winds have died down–for now–and electrical service is slowly being restored, we here in the socialist mecca of Venezuela, oops I mean California, have contained the Zombie outbreak…this time. Consider this a practice run for “the big one.” We, living here in the SMUD service area, did experience 48–mostly arson fires–on the first day of the PG&E blackout but I’m sure it’s just coincidence.

In light of the recent fright that Northern Californians experienced from the PG&E power outages, we here at Really Right noticed that PG&E was experiencing a public relations nightmare over this service interruption. Their local offices were egged, their vehicles were shot, and other acts of vandalism occurred as well. As a result, we felt that PG&E needs to undertake a “feel good” campaign to win back the hearts of customers. In a spirit of sympathy for both PG&E and their customers, we decided to screen potential candidates as the new spokesman for the embattled company.

Our first thought was Chuck Norris. Chuck is well known as a man’s man. He doesn’t seem to be gainfully employed any more, at least not in front of the camera so we thought a financially struggling company could afford him. However, we decided that Chuck is not right for a California based company; especially, one headquartered in San Francisco. Chuck is a manly conservative and isn’t compatible with a company that poured ratepayer money into opposing Proposition 8. Why an electric utility has any business in taking sides on whether marriage should be between one man and one woman is just proof that their management sucks. Also, having Chuck Norris associated with this utility has a bigger problem. You see, nobody turns the lights out on Chuck Norris, Chuck Norris puts their lights out.

Nobody turns out the lights on Chuck Norris

Michael Myers was another thought. What is October without Mike? The State is experiencing a lot of tension due to the fright given to them by PG&E and we are busily prepping for Halloween anyway. Baby Boomers, especially those in office, can really relate to Michael. When they were first dating in junior high, going to one of his movies was a surefire way to get a girl to curl-up in their arms. Oh, what fond memories. Mike has California roots being a well-known commodity in Hollywood. Mike is also known to avoid firearms and favors knives for his “wet work“. Given that our current Governor thinks that law abiding people shouldn’t be allowed firearms, this policy might seem to favor a guy like Michael Myers. However, Mike is known as the strong, silent type and like Chuck Norris, prefers to let his hands do the talking. He is really light on dialogue in his movies and that is a problem when you need a guy for doing voiceovers for commercials.

Michael Myers–light on dialogue

Our third candidate, Freddy Kruger, is strong in areas where Mike Myers is weak. Freddy has a distinctive voice that you never really forget. Freddy also is best known as a guy that reminds you to keep your lights on at night. In fact, Freddy has a following that never wants the lights to go off again. Freddy, unlike Myers, never wears a mask. As a disabled individual, Freddy has really used his disability to make a name for himself. The fact that Freddy is a grossly disfigured burn victim that is thriving amongst ordinary people is inspiring. You never know where he will pop-up next. This fact causes people to pay attention whenever he is on your television. Freddy could be a role model for what PG&E could become. Both have survived a horrible fire and PG&E is learning to overcome adversity and begin life anew. Freddy has been there and done that.

Freddy makes you want to keep the lights on

Some may wonder why I made the connection between Michael, Freddy, and PG&E. And for that, we circle back once again to San Francisco. The progressive leadership in San Francisco wants to dismember parts of PG&E. In some Frankenstein-like way, they want to create their own utility, but unlike a real utility, this one only owns transmission lines and no power generating facilities. I guess that would make it a very “green” utility with no carbon footprint other than that of an occasional fire. PG&E also provides natural gas service to “The City” but no word on who gets that slice of the company.

For those of us living in the real world, this idea makes absolutely no sense; especially, in that city. As the Sith Lord’s father liked to point out, nobody knows what is really under that city. Parts of their infrastructure date back to the Gold Rush era and there are no maps of what lies below the streets of San Francisco. Then there are the parts that survived the 1906 quake which again are not recorded but likely used in some spots. Thus San Francisco has many ancient components of their infrastructure that are in use way beyond their designed life. Taking on this liability is insane on the face of it. The city fathers may very well get their wish and live to regret it as “fire sale” can be defined in more than one sense.

San Francisco during 2017 blackout

Anyway, both PG&E and Freddy Kruger are associated with fright, fires, and dismemberment. It’s a match made in times of adversity, but it just might work. This association will inspire ratepayers to keep the lights on at any price as the alternative is too frightening. We here at Really Right think they ought to take a stab at it.

PG&E was able to accomplish something in the last 24 hours that has not happened since the Loma Prieto Earthquake. They shook all of NorCal to the core. PG&E announced they were going to shut off power to 600-800k homes in Northern California, in 34 different counties. This has been going on, albeit on a much smaller scale, over the last couple months because…well if PG&E is liable when their equipment causes a fire, they should have the right to cut the cord to your electricity. However it was never done on a scale this large, and as a result brought out a plethora of people who are; woke, shook, naïve, and others who get all their news from cable television.

Yikes! Boy is it fun to watch this drama unfold. As a result of watching the impending doom on the 24/7 news station of their choice, people suddenly started worrying that they could be without power for weeks…or that their area was affected…and as predicted by William in this space, panic began to set in. People suddenly began talking around the watercooler about solar power, backup batteries, and generators. Overnight these otherwise clueless people became armchair preppers.

I call these people; woke, naïve, shook, and cable watchers because they take a headline written for a cable news outlet (or their website) by some guy in Atlanta, New York, or Washington, D.C. and blow it way out of proportion.

Run for your lives, they’re cutting the power

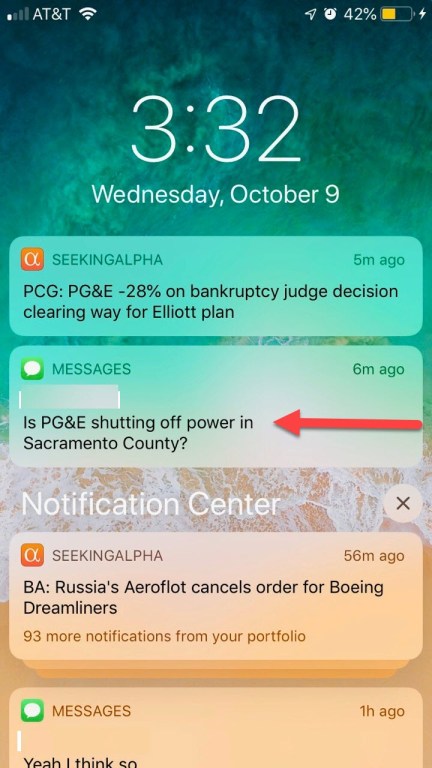

Look at this text message I received…keep in mind if you live in Sacramento County like this guy does, you get your power from SMUD not PG&E. When I reminded him of this, it didn’t deter him in the least. He kept on objecting that it was on television and the radio so it must be true. What I told him didn’t matter; he wouldn’t believe me even after providing him irrefutable evidence.

Is PG&E cutting power in Sac County?

He kept objecting, “But I saw it on the news.” It wasn’t until I finally sent him an official statement from SMUD saying no blackouts are planned that he finally backed down.

(Editor’s note: I heard people voicing similar concerns at work as this was unfolding. People had no clue who their electric provider is even though they pay a monthly electric bill. I was amazed that a graphic used in a television broadcast could so easily override common sense and create such an uproar.)

Another friend of mine in PG&E territory called in a panic. I told her she wouldn’t be affected either as she lives in a heavily populated urban area…still it wasn’t good enough. Even after I sent this person the official map of affected homes from PG&E, this did nothing because she “heard it on the news.”

The blackouts have started and they are only affecting very rural areas so far; think Angel’s Camp, Mokelumne Hill, Mill Valley, and most of rural counties. The crisis has so far been averted; however, on the way home from the gym last night, I stopped at a local Safeway…and found the shelves with bottled water looking pretty bare! Therein lies the problem folks, I live in Sacramento County and it will not be affected by this shut off, yet the people who tuned in to view cable news last night missed that memo.

The general point here being, find a trusted source to get your news. The cable channels specialize in sensationalism and therefore won’t release the story until it creates the necessary drama. Sadly it had its intended result; it stirred up the natives. As a result, a lot of older and just plain naïve people were stirred into a frenzy and scared.

But hey, look at it this way, you spend $200 a month for all those channels even though you can only watch one at a time! Me on the other hand, I don’t need cable. Instead, I get to watch all of you scurry around like cockroaches because you do. That dear readers is entertainment.

Photo: Auburn, CA 10-09-2019 credit Sacramento Bee

For those of us in the shadow of the State Capitol, it’s just another day. However, if you live elsewhere in the State, things are anything but normal.

Shoot the Messenger

A PG&E employee was driving a truck Tuesday evening in Northern California’s Colusa County – before the electricity cutoffs – when a bullet shattered one of the vehicle’s windows, the California Highway Patrol told The Associated Press. The driver was not hurt, according to the AP.

CHP is investigating the incident, which occurred north of the town of Maxwell as the staffer headed southbound on Interstate 5, according to authorities. A white pickup may have pulled up beside the PG&E truck before the shooting, CHP Officer J. Sherwood told the San Francisco Chronicle.

More than a million people in California were without electricity Wednesday as the state’s largest utility pulled the plug to prevent a repeat of the past two years when windblown power lines sparked deadly wildfires that destroyed thousands of homes.

The unpopular move that disrupted daily life — prompted by forecasts calling for dry, gusty weather — came after catastrophic fires sent Pacific Gas & Electric Co. into bankruptcy and forced it to take more aggressive steps to prevent blazes.

The drastic measure caused long lines at supermarkets and hardware stores as people rushed to buy ice, coolers, flashlights and batteries across a swath of Northern California. Cars backed up at traffic lights that had gone dark. Schools and universities canceled classes. And many businesses closed.

Why have forest management when you can just pull the plug at random?

“I wish we weren’t in a situation where, in maybe one of the wealthiest jurisdictions in the world, we are turning power off to large swaths of the population every few weeks,” said Michael Wara, director of the Climate and Energy Policy program at Stanford University. “But it is better than what we’ve been through, and I very much hope that we get through this fire season without a repeat of 2017 or 2018.”

PG&E declared bankruptcy in January, in part because of potential liabilities from its role in some of the 2017 northern California fires and the 2018 Camp fire that killed a total of 129 people and destroyed tens of thousands of homes.

“Is it a huge inconvenience? Yes. Is it going to be dangerous? Yes,” Wara said. “There are lots of risks on the other side. Someone could die because they have a medical device.

PG&E should have been maintaining and updating its infrastructure before the crisis reached this point, said Mindy Spatt, a spokeswoman for the Utility Reform Network.

“PG&E should be held to higher standards than this,” she said. “No one wants to see another fire like the fires we’ve seen in the past, but we have to remember that the problem that these shutoffs are hopefully going to address are PG&E’s negligence and incompetence, and PG&E’s propensity to ignite fires.”

Now PG&E customers must bear the burden of navigating possibly days without power, with businesses losing money and people in possibly unsafe situations, Spatt said.

“Consumers would rather have their power shut off than have their homes and businesses burnt down, but they would also rather have a utility that didn’t start fires,” Spatt said.

The shutoffs are part of its wildfire mitigation plan, mandated by the state and agreed to by the California Public Utilities Commission, the state’s top power regulator. — Kevin Stark

Folks, when you live in a socialist state, you get socialist utilities too. We keep being told the lie by the ruling class that wind and solar are the way to energy independence so what happens on a sunny, windy day—conditions that we are told are best for energy production—why we cut the power off to people in the state’s flyover country.

But elites take care of their own. Tesla is prominently mentioned in two articles that I saw about the scheduled blackouts yesterday.

One article mentioned that the scheduled outages stopped just short of Tesla’s production facility in the San Jose area and the other was to juice-up before the lights go out.

The electric automaker issued a preemptive over-the-air advisory overnight to many vehicle owners, telling them to charge up ahead of the planned outages, which utility Pacific Gas & Electric began rolling out Wednesday to try to lessen the risk of wildfires.

“A utility company in your area announced they may turn off power in some areas of Northern California beginning October 9 as part of public safety power shut-offs, which may affect power to charging options,” the message read, according to social media posts. “We recommend charging your Tesla to 100% today to ensure your drive remains uninterrupted.”

So what ever happened to Elon’s promise that his cars could be charged as they were driven by solar cells built into the car? Actually, Toyota was promising something similar a few years ago but I digress…

I still haven’t heard whether Oakland participated in the lights out festivities.

Closing Comments

All of this bowing to the environmentalists goes back to the oil spill in Santa Barbara back in 1969. Up until that happened, nobody cared about the environmentalists. From that point forward, they increasingly gained access to influence public policy in California. Now nobody dares to act without their blessing.

Environmentalists purposely destroyed the logging industry in California and now we have tens of millions of dead and dying trees in our forests and nobody to cut them down. This is why we have decades of fuel gathering on the forest floor.

Dead and diseased trees in California #1

While PG&E did spark some fires, many in our State are the result of arson and nobody has been arrested for most of the manmade forest fires.

Dead and diseased trees in California #2

Any way you slice it, government failure is to blame for the current mess.

As predicted, Governor Newsom signed AB 1482 into law yesterday at a ceremony in Oakland. Any rental properties still standing when PG&E turns the power back on will be subject to this law beginning January first. The fact that this is a huge power grab by state officials and that voters just rejected a similar measure be damned.

Folks, this is just a fancy way to keep poor people poor and enhance the portfolios of the rich. You see, in recent history, the best place to get a return on your investment has been Wall Street. Arguably, the stock market is overvalued and there are some bubbles in various sectors that increase the risk of investing. Now, rich Liberals can invest in corporations that specialize in rent control properties and boutique housing in Oregon and California and get 25 times (not a typo) the return that you can get in a bank savings account, risk free and guaranteed forever. This revenue stream increases each year, plus they get a cost of living increase to keep ahead of inflation as well. This diversifies the savings of the rich and has a better return than traditional “Blue Chip” investments.

Folks when you hear that Warren Buffett gets rich on the backs of the poor, its stuff like this that he uses to gain and keep his wealth. If managed properly, any investment in a rent control scheme will double your money about every decade.

Here’s how Buffett does it:

Once the property needs maintenance, you can increase your wealth even more. You sell the rental property from Corporation A to Corporation B, both of which you own. Corporation B, fixes up the property using a third corporation that you also own to do the capital improvements. Once modernized, you can then increase the rent to current market values and then get new tenants and repeat the cycle.

Since nobody on the low end of the income ladder gets five percent wage increases each year plus a cost of living adjustment, the poor will get even poorer while the rich get richer.As an added bonus, at election time, the rich Liberals will play the class envy card and blame Republicans for the plight of the poor which they engineered.

In an historic first, humanity has been given advance warning that the Zombie Apocalypse is scheduled to begin tomorrow. Contrary to earlier reports, the evil corporate entity responsible for the end of life as we know it is not the Umbrella Corporation.

Umbrella Corp logo

Instead, government officials have announced that the responsible entity is a bankrupt company bent on self-preservation at the expense of humanity and what passes for civilization in this once Golden State. Enter one Pacific Gas and Electric Company. No not the cheesy 1960’s rock band but the once proud public utility.

Rock band Pacific Gas and Electric

The spark responsible for the anticipated chaos is the purposeful and simultaneous loss of electrical power in 30 California counties. The affected areas are expected to include Silicon Valley and peace loving Oakland.

PG&E 30-county blackout area

Here is the completed list of affected counties:

Alameda, Alpine, Amador, Butte, Calaveras, Colusa, Contra Costa, El Dorado, Glenn, Lake, Mariposa, Mendocino, Napa, Nevada, Placer, Plumas, San Joaquin, San Mateo, Santa Barbara, Santa Clara, Santa Cruz, Shasta, Sierra, Solano, Sonoma, Stanislaus, Tehama, Tuolumne, Yolo and Yuba

San Francisco blackouts expected here

Personally, my money is on the Raider’s fans to be the backbone of the lawlessness which will ensue; especially, if the blackouts go into overtime.

Raider fans eager to do their part

If this materializes as promised, look for Silicon Valley folks to transfer critical operations to other states with cheaper and more abundant power and less government red tape.

Oh, and here is a typical newsfeed of the warning being broadcast.

Pacific Gas and Electric Co. is warning customers that the utility may shut off power to 30 California counties this week because of a potentially widespread wind event.

The potential Public Safety Power Shutoff could impact more than 600,000 customers across Northern and Central California, the utility said Monday night.

The strong and dry wind event, forecast for Wednesday morning through Thursday afternoon, could impact much of PG&E’s service area, which includes northern, coastal and Bay Area counties. The National Weather Service has issued a fire weather watch for midweek.

“If PG&E decides to implement a PSPS, the company expects to begin turning off power for safety early Wednesday morning,” the utility said Monday night.

If you live in one of these areas stock up on water and shotgun shells today.

Oh to identify the zombies, look for the stranger carrying your neighbor’s television set or dragging his wife down the street towards their gasoline powered vehicles. Zombies don’t drive Tesla’s in PG&E service areas.

Raiders fan rehearsing for Zombie Apocalypse

Stay tuned to this blog for further developments as the situation warrants.

When it comes to business and entertainment, China seems to be dictating American policy. Just as they govern their own nation with fear, American companies are succumbing to fear of the Dragon of the East. When given a choice, Americans are choosing profit over principle every time.

China has made a huge investment in Hollywood over the last several years. As a result, they have actively reshaped the plots and casting of many big budget movies. Sometimes the changes made headlines and other times it hasn’t. One of the earliest changes that I recall was the remake of Red Dawn.

Red Dawn 1984

In the original 1984 movie, troops from Cuba and Russia make a surprise attack on the United States and get bogged down in a protracted fight. A group of high school students wage a guerrilla war against the invader’s supply routes.

As Hollywood often does, they remade the movie in 2012. Since the Soviet Union had fallen decades before, they needed a new villain, an aggressor nation with the military might to take on the United States. The logical choice was China. However, a curious thing happened in the midst of post-production. The studio nixed the China thing and made the producers change the aggressor nation to North Korea.

Red Dawn 2012

Was China originally the country invading the USA?

Yes, the People’s Republic of China (PRC) was originally presented as the invading regime, but after pressure from the PRC government and studio concerns on how it could impact the international box office, the film was digitally altered in post-production to replace all the PRC flags, posters and dialogue with that of North Korea.

Since then, it has become commonplace to change scripts or edit movies in such a way to get distribution in China. Even Hollywood “tent pole” movies like the Avengers have been altered to make it marketable in China.

Such changes are just the tip of the proverbial spear.

Today, two more news stories about compromising to please China are in the headlines. First up, the National Basketball Association (NBA).

The headline from ultra-rightwing publication Rolling Stone says it all.

In a Friday night tweet that he has since deleted, the Houston Rockets general manager expressed support for the legions of protesters who have taken to the streets of Hong Kong.

However, the problem for Morey is that the Chinese also love basketball. And thanks surely to the stardom of former Rockets great Yao Ming — now the head of the Chinese Basketball Association — Houston trailed only Golden State in popularity in the nation, per a recent survey. There appears to be too much money to be made in China for the NBA to stand up for human rights.

Yao himself responded to Morey’s tweet with condemnation, calling it “an inappropriate comment related to Hong Kong” and the CBA suspended its “exchanges and cooperation” with the Rockets. Chinese sportswear maker Li-Ning did the same, suspending its association with the team. The Chinese government also weighed in via its consulate, saying that it was “deeply shocked” by the tweet. The Rockets owner, Tilman Fertitta, quickly disowned Morey’s tweet:

Listen….@dmorey does NOT speak for the @HoustonRockets. Our presence in Tokyo is all about the promotion of the @NBA internationally and we are NOT a political organization. @espn https://t.co/yNyQFtwTTi — Tilman Fertitta (@TilmanJFertitta) October 5, 2019

The Rockets and the NBA could have stood up for Morey, for decency, and for the protesters and their human rights.

The NBA issued a sorry statement, declaring the league realizes that the tweet may have “deeply offended” Chinese fans and that they “have great respect for the history and culture of China,” as if that had anything to do with a bill that could be used to disappear journalists and critics of an autocratic regime. Morey, who The Ringer reports was at one point in jeopardy of losing his job, tweeted his own apology that read like it was dictated by his boss. Brooklyn Nets owner Joe Tsai, a co-founder of Chinese e-commerce conglomerate Alibaba, published an open letter on Facebook that referred to protesters as a “separatist movement.” Even James Harden, the Rockets’ star guard, issued a mea culpa for some reason, even though he wasn’t involved.

That last bit of rank submission to an autocratic regime captured the full extent of the NBA’s sellout to China. Several politicians on the left and right, including presidential candidate Julián Castro and Rep. Ben Sasse (R-MO), called out the NBA’s cowardice. Even Rockets fan Ted Cruz took a principled stand:

We’re better than this; human rights shouldn’t be for sale & the NBA shouldn’t be assisting Chinese communist censorship. — Ted Cruz (@tedcruz) October 7, 2019

Wow. Folks when Rolling Stone is singing the praises of Ted Cruz, you know that something is seriously wrong.

The next story probably won’t make it to your INBOX but it goes much the same way. Before getting into the particulars here’s a few nuggets of background. eSports is a big thing in a small segment of popular culture. This is where aspiring kids go to make millions of dollars playing video games competitively. A big hub of this activity is South Korea. Blizzard Entertainment was purchased a few years ago by Activision. Blizzard is best known for their World of Warcraft game. Hearthstone is a virtual card game that is modeled after Warcraft type characters.

Blizzard’s Hearthstone

The popular player ended a recent livestream with a call for his country’s liberation in a post-game interview. “Liberate Hong Kong,” Ng Wai said. “Revolution of our age!”

During the Hearthstone Grandmasters stream, the Hearthstone Pro was wearing a mask similar to those used by rioters in Hong Kong.

After the livestream ended, Ng Wai was immediately removed from the game’s Grandmasters rank and the developer is currently withholding his tournament prize money. The player also received a 12-month ban from the game’s professional events. The player will be unable to participate in Hearthstone eSports until October 5th 2020.

Unfortunately, government interference within China is a constant issue for its citizens. Even amongst the horrendous police brutality shown within the Hong Kong riots, the country still finds time for rampant censorship. With some developers being destroyed for slight anti-government inclusions, Blizzard’s huge Chinese presence does need to be protected in a business standpoint. From a moral and ethical standpoint, however, Blizzard is certainly not looking good.

For those of you that self-identify as low information voters, this is why I have problems with the way we conduct business with China. This also should help explain why I support President Trump’s efforts to change our relationship with China. Do I agree with everything Trump does with China? Probably not, but his instinct is correct. America businesses that put profit over principle are behaving shamefully.

These next two stories hit so many different strands of product liability and malfeasance for Tesla that I couldn’t pass them up. Photos are from the respective articles quoted below. Oh, and NHTSA is National Highway Transportation Safety Administration.

It was just days ago that we reported that the NHTSA was opening an inquiry into the use of Tesla’s “Smart Summon” feature. Then, just hours ago we followed up by reporting that a petition had been filed with the NHTSA claiming that Tesla was using over the air software updates to cover up dangerous battery issues.

Today, we offer a stark reminder that just because the NHTSA has started to perk up its ears, doesn’t mean that Teslas haven’t stopped going up in flames all over the world. The most recent example comes from Austria, where after a Tesla was involved in an accident and caught fire, firefighters had to use a special container to transport the remains of the vehicle and the battery.

Tesla fire

According to a translated version of this ORF News story, a 57 year old driver lost control of his Tesla and crashed into a tree, after first hitting the guardrail. It was then that the vehicle caught fire.

The driver was lucky, as “people passing by the scene of the accident took the man out of the vehicle and called emergency services.”

Firefighters extinguishing Tesla fire

Tesla after fire

In order to put out the fire, the street had to be closed and fire authorities had to bring in a container user to cool the vehicle. The container held 11,000 liters (11 tons) of water and was designed to eliminate the biggest risk in an EV accident which is the battery catching fire.

The Tesla battery is mounted on the underside of the vehicle and contains acids and chemicals that can easily escape during a fire, placing the firefighters in danger.

Tesla loaded into bath tank

Here is the problem: according to the article, some 11,000 liters of water are needed to finally extinguish a burning Tesla but an average fire engine only carries around 2,000 liters of water.

Fire brigade spokesman Peter Hölzl warned that the car could still catch fire for up to three days after the initial fire.

Bath tank to insure car doesn’t re-ignite

The container used is said to be suitable for all common electric vehicles. It measures 6.8 meters long, 2.4 meters wide and 1.5 meters high, it is (obviously) waterproof and weighs three tons.

We have previously documented the failure of Tesla’s Smart Summons on the blog and now we learn of another issue about Tesla batteries which I will get to in a moment. Then the hazards faced by firefighters. Why does Europe have a full immersion bathtub for electric vehicle fires, and nobody here does? You did catch the part about a Tesla can catch fire up to three days after an accident? I bet that little nugget isn’t in the owner handbook.

Here’s part of the battery story.

A notice published on Tuesday by the NHTSA said they had received reports about a possible defect in Tesla battery packs that could cause fires. The battery packs affected reportedly received new management software as part of over the air updates that were issued by Tesla in May.

The petition was filed by the Law Offices of Edward C. Chen, a California law firm representing a number of Tesla drivers in the U.S., according to Bloomberg.

Chen argued that Tesla is using software updates to cover up a potentially wide spread and dangerous issue: “Tesla is using over-the-air software updates to mask and cover up a potentially widespread and dangerous issue with the batteries in their vehicles.”

Chen has also argued that Tesla owners “saw the range of their Teslas on a charge fall by 25 miles (40 kilometers) or more after Tesla released two battery software updates beginning in May.”

The notice states: “The petitioner alleges that the software updates were in response to a potential defect that could result in non-crash fires in the affected battery packs and that Tesla should have notified NHTSA of the existence of this potential defect and conducted a safety recall. The petitioner also alleges that this software update reduces the driving range of the affected vehicles.”

Folks, I keep saying that the moment the government subjects Tesla to the same standards as other automakers that they are in for a world of hurt. Thankfully that day may finally be approaching.

Electric vehicles are a novelty not a solution. In a fair and free market, they would all but disappear. We tried electric vehicles a century ago and they failed in the market. It would take much more than cheap and abundant electrical power to make them mainstream. The proof that such a day is still far from us is the insistence of politicians and environmentalists that wind and solar are the answer.